Ever pay for coffee, then spot an extra line on the receipt? It’s easy to feel like the total jumped out of nowhere. In most cases, those extra charges are tied to the way card and payment systems work.

Banks, payment networks, and fraud checks all have costs. Merchants usually pay them first, then you may see them as a higher total. In 2026, fee rules and e-commerce risk pricing keep shifting, so the “why” can feel even more confusing.

The good news: once you know the main fee drivers, you can spot patterns fast. You’ll also learn how to choose payment options that tend to cost less, without playing guessing games.

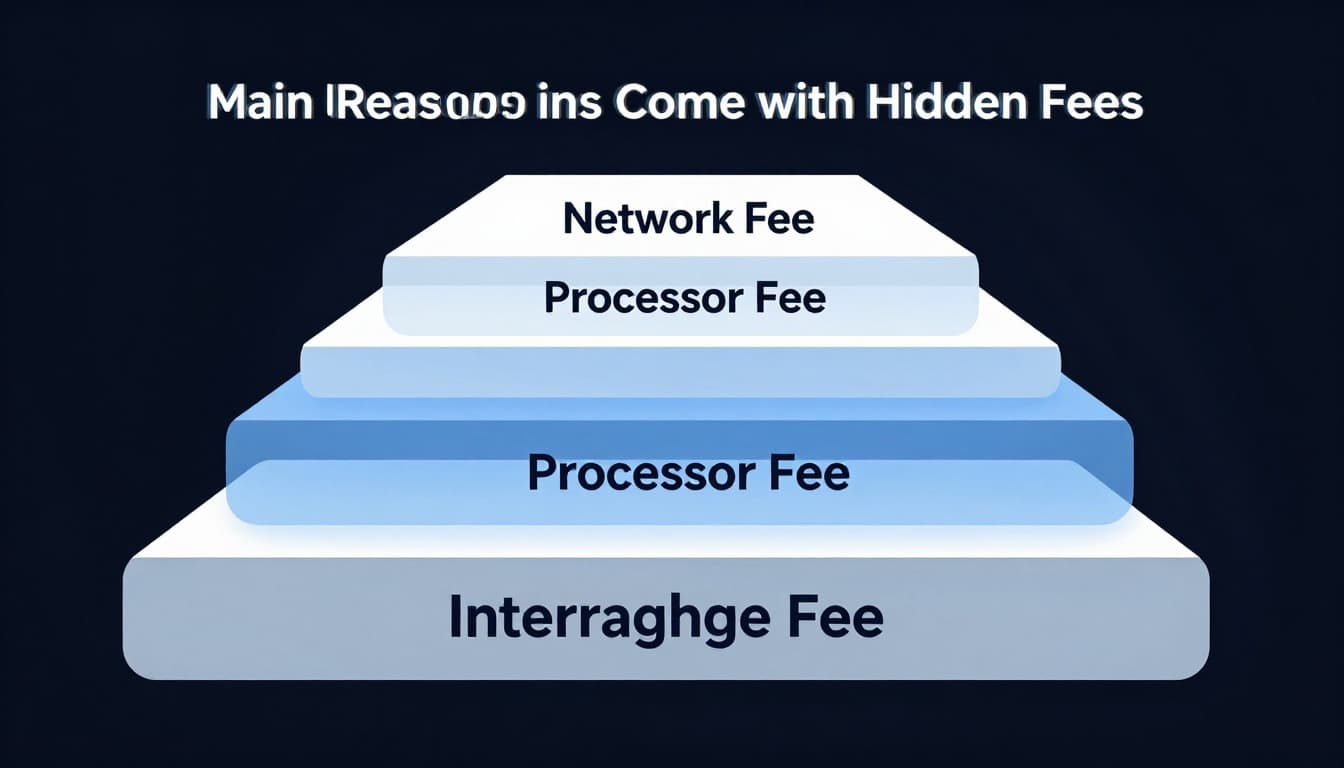

The Main Reasons Transactions Come with Hidden Fees

Think of card payments like a cover charge at a busy club. Even if you pay one person at the door, multiple groups get a cut behind the scenes.

Most “extra charges” come from a few core costs. Here’s the simple version:

- Interchange fees: paid to the card-issuing bank (often tied to rewards and fraud risk)

- Processor markups: what the payment handler charges to move money

- Network fees: costs charged by card networks for routing the transaction

- Risk premiums: higher fees when a payment seems harder to verify

If you want a deeper breakdown of interchange, see interchange fees explained by Corepay.

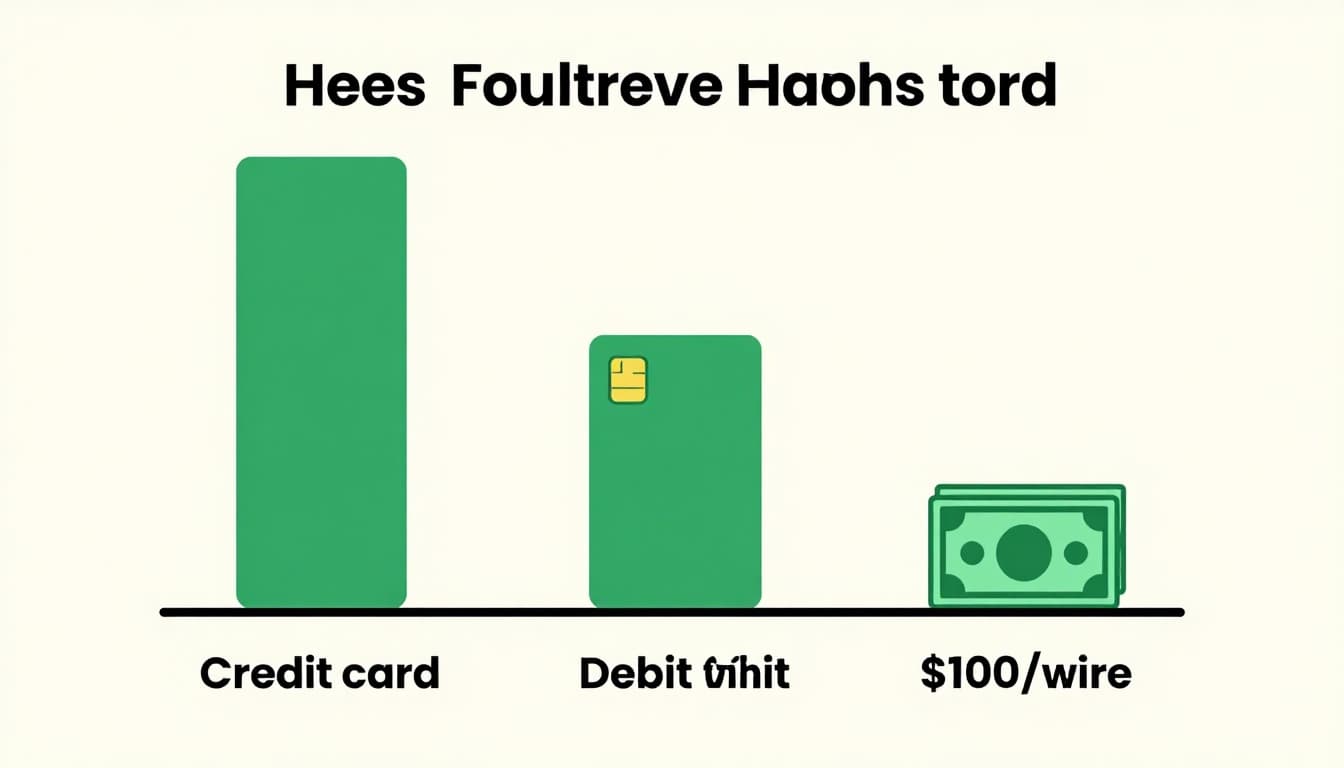

To make it feel real, look at typical U.S. merchant costs for a $100 transaction:

| Payment type (typical) | Avg fee for a $100 transaction (merchant cost) | What it usually covers |

|---|---|---|

| Card purchase (average) | $1.50 to $3.50 (1.5% to 3.5%) | Interchange plus processor and network costs |

| Debit-style card purchase | ~1.5% to 2.9% or less | Regulated debit rates, fewer rewards costs |

| Outgoing wire transfer | $15 to $50 flat | Bank-to-bank speed and manual processing |

Bottom line: the fees often stack, so you don’t see the parts. You just see the final number.

Interchange Fees: The Big Cost for Card Rewards

Interchange is one reason rewards cards can seem “free” to you. Your bank uses part of that fee to fund cashback, points, and chargeback handling.

In 2026, rewards and premium cards still cost more because the demand for points stays high. Based on recent U.S. examples, Visa card-present credit can fall around 1.51% + $0.10. Rewards categories can run higher than basic cards.

So what does that mean for “extra charges” you see? When a merchant faces higher interchange, they often try to keep margins by charging more, even if they don’t call it “interchange.”

This is why a $100 card sale can cost the merchant much more than it looks at first glance. If you’ve ever wondered why some payments feel “priced in,” interchange is the most common answer.

Also, in 2026 Visa made updates that affect small business rates and program handling. Some changes began in January 2026, and additional shifts roll into the year. That can quietly change totals even if the merchant didn’t change anything on their end.

Processing and Network Add-Ons That Pile Up

Even after interchange, you still have other costs. The processor has infrastructure costs (hardware, routing, reporting). The network charges for moving the transaction through its rails.

These costs can matter most when payments are riskier or more complex.

Also, payment types can trigger different fee paths. For example, card-not-present transactions (online checkout) often face higher risk reviews than card-present transactions (in-store). When you add “proof” steps, the fee math can change too.

Meanwhile, digital wallets can affect how transactions are verified. Tokenization can reduce some fraud exposure, but it doesn’t remove all costs. It just changes how the risk is assessed and billed.

In short, extra charges are rarely one fee. They’re usually a chain of costs you never asked to understand, but you end up paying for anyway.

How Fees Change Based on Your Payment Choice

Not all payments are priced the same. That’s why two people can buy the same thing and see different totals.

For a quick comparison on $100, here’s how the averages tend to move:

| Payment choice for a $100 purchase | Avg fee to merchant (typical) | Why it tends to cost that way |

|---|---|---|

| Card purchase (in-person) | ~1.5% to 3.5% (varies) | Rewards funding plus fraud checks |

| Online card purchase | often higher than in-store | More risk because no physical card |

| Debit-style card purchase | ~1.5% to 2.9% or less | Lower rewards cost, regulated parts |

| Outgoing wire transfer | $15 to $50 flat | Speed and bank handling fees |

Credit Cards: High Fees for Convenience and Protection

Credit card fees often run higher because rewards and fraud protection sit inside the pricing. For in-store transactions, Visa examples can land near 1.51% + $0.10. For online, risk can push costs up.

Recent U.S. data shows non-qualified online transactions around 3.15% + $0.10. In other words, the same card can become “more expensive” once it’s not in your hand.

That also explains why you sometimes see fee lines at checkout, or why some merchants offer cash discounts. They’re trying to avoid the higher cost of card-not-present risk.

If you want an overview focused on business-side costs, NerdWallet’s guide to credit card processing fees is a helpful starting point.

Debit Cards: Regulated but Watch the Extras

Debit cards usually cost less because the regulated parts can cap certain interchange rates. In example schedules, “pin debit” can be around 0.05% + $0.21, which comes out near $0.71 on a $100 purchase.

However, “cheaper” doesn’t always mean “fee-free.” Some debit transactions still use signature mode and can cost more. Also, international transactions can increase costs due to different risk and processing rules.

So if you’re trying to reduce extra charges, debit is often a smarter bet. Still, always check whether the merchant has a card surcharge policy.

Wires and Transfers: Paying for Instant Speed

Wire transfers are built for bank-to-bank movement, not small retail purchases. That’s why the fee style looks different. Instead of a percent fee, outgoing wires often come with flat fees, commonly $25+. Incoming wires may be free or cost around $10, depending on the bank.

If a store is offering you a “wire” option for something that should be a normal purchase, that’s a red flag. The fee structure is designed for large, high-value transfers, not everyday spending.

Also, international transfers can bring extra conversion costs. So the price can grow beyond the wire fee itself.

Merchant Surcharges: When Stores Pass Fees to You

Sometimes the extra charge isn’t a mystery network fee. It’s a merchant surcharge, which means the store adds a card fee to your total.

Whether it’s allowed depends on state rules and card network requirements. In general, merchants often must disclose surcharges clearly, and some systems cap how much they can charge. For example, Visa rules can allow surcharges up to a 4% cap when properly disclosed.

Because laws vary, it helps to check a current state-by-state summary if you’re dealing with a business that posts these fees. This reference on credit card surcharge laws by state is one option to understand the landscape.

If you want a practical tip, look for a surcharge notice before you pay. If the notice is missing, question it politely. Many merchants bake the cost into the price instead, so you won’t always see it.

Gotcha: surcharges are not the same thing as your bank’s card fee. They’re usually the merchant passing along acceptance costs.

Ways to Dodge Extra Charges in 2026 and Beyond

You don’t have to avoid cards entirely. Instead, aim for payment choices that tend to reduce fees and risk.

Here are practical moves that work in 2026:

- Choose debit with PIN when it fits the situation. Regulated PIN debit often has lower rates than many credit-like paths.

- Use ACH over wires for moving money, especially for bills and transfers. Wires tend to be priced as “pay for speed.”

- Pick in-store over online when you can. Online card-not-present can cost more due to added risk checks.

- Use secure checkout options like 3D Secure when prompted. Extra verification can reduce risk classification.

- Ask about cash discounts at small businesses. Some places lower totals for cash to avoid card acceptance costs.

- Review your statement for any card-not-purchase fees (like dispute or foreign transaction fees) so you separate bank charges from merchant surcharges.

- If you run a business, ask processors about interchange-plus pricing. Transparent models can reduce how much you pay. See interchange-plus pricing explained in 2026.

Even if you only adjust one routine purchase, the savings can add up over a year.

Conclusion

Extra charges on transactions usually come down to risk, rewards, and speed. Interchange fees fund rewards and fraud handling, while processor and network add-ons stack on top.

Fees also vary by how you pay. Online card purchases often cost more than in-person ones, and wires tend to be pricey for smaller transfers.

If you want one action to start this week, do it now: check where you see the fee, then switch to the payment option that usually costs less in that moment. With a few smart swaps, you can keep more of your money.