The next time you buy coffee online, ask yourself one question: how does your money get from your account to the seller so fast? Most of the time, the answer is not magic. It’s a set of behind-the-scenes steps that move along in a tight order, usually in minutes to a few days.

When you pay by card, bank transfer, or wallet, your payment follows a path. That path includes your bank, the seller’s bank, payment networks, and payment processors. Even though the customer experience feels instant, the system still checks risk, swaps transaction info, and then moves funds.

So, how a payment moves from your account to a seller comes down to four common phases: authorization, clearing, settlement, and payout. Along the way, security controls help protect your data and confirm you’re really the payer.

In the sections below, you’ll see each phase in plain language. Then you’ll learn how the path changes for cards, ACH, and wallets. Finally, you’ll get the 2026 update on real-time payments and what security looks like today.

The Core Steps Every Payment Takes Behind the Scenes

Think of a payment like a relay race. Each runner does one job, and the baton has to pass at the right time. If a runner drops the baton, you might see a decline or a delay.

Across most payment types, the universal flow looks like this:

- Authorization: Your bank checks if funds (or credit) are available.

- Clearing: Banks and partners exchange transaction details.

- Settlement: Money actually transfers between financial institutions.

- Payout: The seller receives the funds (minus fees, if applicable).

This three-part lifecycle is often described as the backbone of card payments. If you want a clear walkthrough of the terms, see authorization, clearing, and settlement from Payment Streets.

To make this feel more real, here are the key players you’ll hear about:

- Your bank (issuing bank): It issues the card or holds your account.

- Seller’s bank (acquiring bank): It works with the merchant to accept payments.

- Payment processor: Companies like Stripe or Square help route and manage transactions for the business.

- Payment network: For cards, networks like Visa or Mastercard help carry the message.

- Payment gateway: For online payments, it captures your payment info and helps send it securely.

Here’s a simple “phase diagram” in words:

Authorization (approval check) → Clearing (details exchange) → Settlement (money movement) → Payout (merchant receives)

Next, let’s zoom in on each phase, starting with the quick yes or no you never really see.

Authorization: The Quick Yes or No

Authorization happens in seconds. That speed matters because it’s the moment the system decides whether the payment can go through.

When you enter card details (or confirm a transfer), the payment request routes to the seller’s payment setup and then to your issuing bank. Your bank checks things like:

- Funds or credit availability

- Account status (is it active and in good standing?)

- Risk signals (is this payment pattern unusual?)

At this point, no money moves to the seller. Instead, the issuing bank sends back an approval or decline. Sometimes, the system also creates a temporary hold.

If you’ve ever seen “pending” on a card purchase, that’s often what you’re looking at. The charge is authorized, but settlement hasn’t finished yet.

For online payments, you may also see extra steps for card-not-present transactions. This is where authentication helps reduce fraud. If your payment fails an authentication check, the system may decline it to protect you and the merchant.

Also, notice the difference between “approved” and “completed.” Authorization is an agreement in principle. Settlement is when the actual transfer occurs.

So, authorization is the gatekeeper. It checks your ability to pay fast, before the rest of the payment relay runs.

Clearing and Settlement: Swapping Data and Funds

After authorization, the payment still needs follow-up steps.

Clearing is the paperwork and details exchange. Banks, processors, and networks share the transaction records so each side agrees on what happened. This includes things like the amount, timing, and identifiers for the payment.

Settlement is the money movement. Here’s the big idea: settlement can’t happen until everyone agrees on the final totals and rules. That’s why settlement often follows clearing by a short window.

In many card and ACH flows, settlement can happen within about 1 to 3 business days, depending on the payment type and cutoffs. Sometimes it’s faster. Sometimes it batches up.

For a deeper look at what “settlement” means and how timelines work, check how payment settlement works and timelines.

A helpful way to picture this is “batching.” Instead of moving every dollar the instant a transaction is authorized, systems often process groups of payments. That keeps operations stable and reduces errors.

If you want a practical takeaway, remember this:

- Authorization feels instant

- Settlement can take time

- Payout depends on settlement

So even when you buy something today, the seller’s bank may not receive final funds until the clearing and settlement steps finish.

Payout: When the Seller Sees the Money

Now the final handoff happens.

Payout is when the seller’s account actually reflects the funds from the transaction. The timing depends on the same factors that affect settlement, plus the seller’s payment setup.

A few things can change when a merchant sees money:

- Payment method rails (cards versus ACH versus instant rails)

- Processor schedules and fees

- Bank processing days

- Whether the payment was fully completed or still pending

For many card purchases, the seller might see funds within 1 to 3 days after authorization, after the clearing and settlement work finishes. For ACH, settlement is often slower, but costs can be lower.

In some cases, a seller may receive funds sooner because of the processor’s funding models. Other times, payouts follow a schedule set by the processor and merchant account terms.

That’s why your experience can show “approved” quickly, while the seller’s cash-in might lag behind.

Next, let’s talk about how the path changes depending on how you pay.

Payment Paths: Cards, ACH, and Wallets Explained

The core phases still exist no matter how you pay. However, the timeline and the “shape” of the path change.

Here’s a quick comparison of typical timing and cost patterns in the U.S.:

| Payment method | Typical time to seller | Typical fees (merchant-facing) | Common use |

|---|---|---|---|

| Cards (debit/credit) | 1-3 days | 2-3% (often + fees) | Retail, online checkout |

| ACH (bank transfer) | 2-5 days | Lower fees | Bills, invoices, payroll |

| Wallets (PayPal, Apple Pay, Venmo) | Instant to 2 days | Varies by wallet/deal | Faster checkout, P2P or online |

Real results vary by merchant size, processor terms, and bank behavior. Still, the patterns above explain why businesses choose different methods.

Now, let’s break down the three common paths.

Credit and Debit Cards via Visa or Mastercard

When you pay with a card, your payment usually goes through a familiar chain:

Buyer card payment → gateway → processor → network → issuing bank

Authorization is the fast check that decides whether the card transaction can proceed. Then clearing and settlement follow, often in batches.

For card purchases, you’ll usually notice:

- Fast approval at checkout

- “Pending” status until settlement posts

- Merchant fees that can be higher than ACH

If you want a practical, plain-English view of what card processing means, see credit card processing explained. It’s a good reference when you’re trying to translate the terms you see on merchant statements.

Overall, card payments are popular because they work for many types of purchases. They also include strong authentication options, especially for online transactions.

ACH Transfers: Straight Bank to Bank

ACH is usually slower, but it can be cheaper.

Instead of using card networks, ACH moves money through the ACH system between banks. That matters because it changes the timing model. ACH often relies on batch processing and settlement windows.

ACH is a strong fit when the payment amount is predictable. It’s also common for recurring bills and invoices.

Compared to cards, ACH often brings:

- Lower fees

- Fewer card-related disputes

- No card number needed

- Longer timelines

If you’re weighing costs, this guide on ACH vs credit cards breaks down why some businesses choose ACH for recurring payments.

So, for ACH, your money still goes through checks and confirmations. But the actual movement of funds tends to happen on a slower schedule than cards.

Digital Wallets Like PayPal, Apple Pay, or Venmo

Wallets add a layer.

When you pay with a wallet, the wallet can store your payment method details. That lets you checkout faster. It also means the seller might not directly handle your card number.

Depending on the wallet and the payment type, settlement can look more like:

- Card settlement (if it’s backed by a card)

- ACH settlement (if it’s linked to a bank account)

- Instant transfers (if it routes to real-time rails)

Wallets also change the experience for person-to-person payments. For example, Venmo can move money between users much faster than traditional bank transfers, depending on account settings and network support.

In short, wallets usually speed up checkout. Meanwhile, your payment still ends up using bank rails, card rails, or real-time rails to finish settlement.

Next, here’s where 2026 matters: payments are getting faster in a new way.

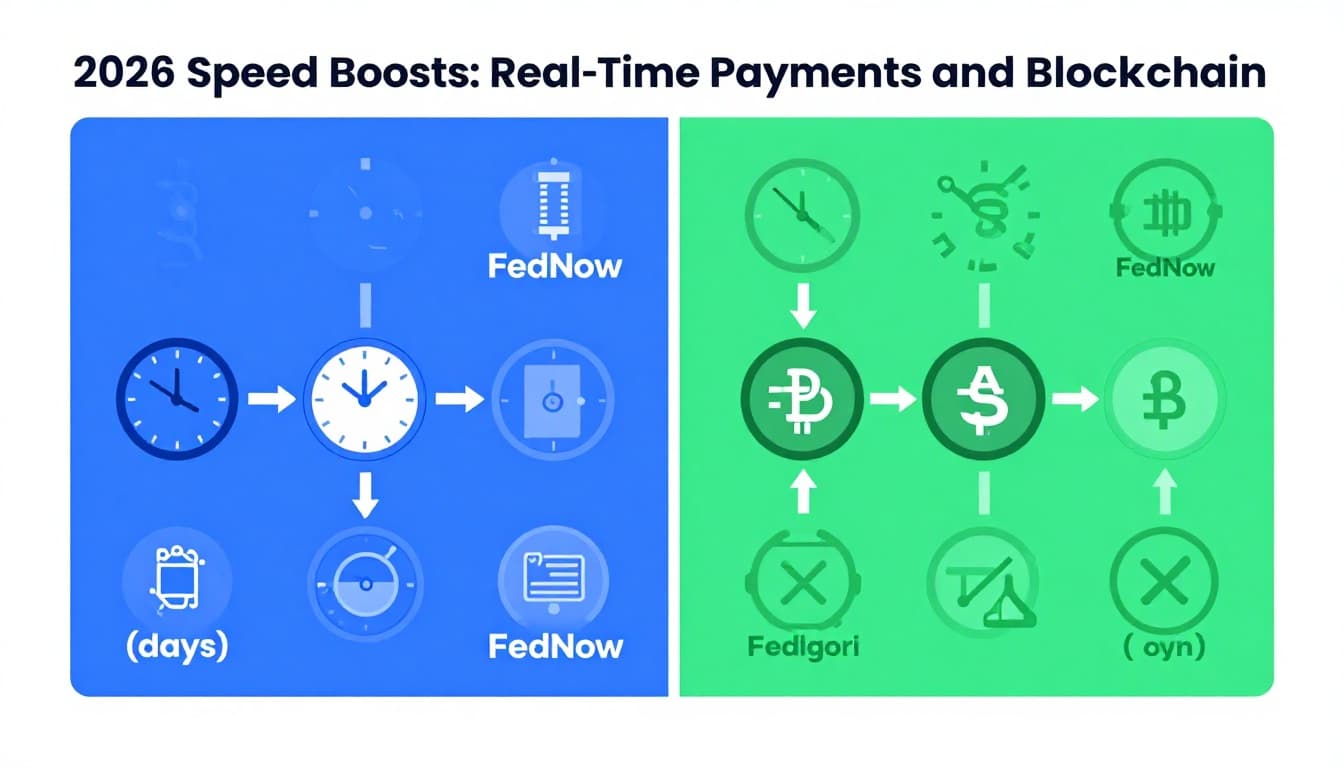

2026 Speed Boosts: Real-Time Payments and Blockchain

For years, “instant” mainly meant approval at checkout. Now, instant is spreading to settlement too.

In the U.S., real-time payment networks help move money 24/7. Two key systems are FedNow (Fed-created) and RTP (The Clearing House). By early 2026, adoption is growing fast.

Here are some real numbers based on recent reporting:

- FedNow has over 1,400 U.S. banks and credit unions joined by early 2026.

- RTP has over 1,100 participants, with broad reach through major institutions.

- Many institutions are still in a receive-only setup. That means not everyone can send instantly yet.

For a sense of how real-time payments are moving from growth to execution, see real-time payments reach a turning point in North America.

Another sign of momentum: PYMNTS reported 58% of U.S. banks use both RTP and FedNow for instant payments. You can read 58% of US banks use both RTP and FedNow.

How “instant” changes the payment journey

With real-time rails, the clearing and settlement steps compress. You still have checks and messaging. But the time from approval to cash availability shrinks a lot.

So the four phases still exist. The difference is that more of the relay happens quickly, not after a batch cutoff.

Where blockchain fits in (and what it doesn’t)

Blockchain payments are growing too, especially for cross-border and business-to-business use.

The main idea is simple: instead of relying on banks to update ledgers, a blockchain network records transfers. That can speed up settlement, especially between compatible systems.

In the U.S., major payment players have been moving toward stablecoin and blockchain support. For merchants, that can mean getting paid quickly in a digital form, then converting later if needed.

That said, blockchain is not “universal instant money” for every checkout yet. It depends on whether the merchant, processor, and customers support it.

The bigger picture is clear: 2026 is pushing more payments closer to real-time settlement. Next, let’s talk about the part people worry about most, security.

How Security Protects Your Payment Every Step

Payments feel safe when multiple controls work together.

Security starts before you submit a payment. It continues through authorization. It also protects the data while it moves between parties.

Here’s what commonly helps protect your payment journey:

- Encryption and tokenization: Your system hides card numbers and protects data in transit.

- 3D Secure (card authentication): It helps verify cardholders for online purchases.

- Biometrics (in wallets): Face ID or fingerprint can add an extra approval layer.

- AI fraud detection: Risk models flag odd patterns before money moves.

- EMV 3-D Secure updates: Newer versions aim to reduce friction without lowering protection.

If you want an authoritative look at EMV security direction, see EMV 3-D Secure in 2026. It explains why standards matter for authentication and safer payments.

For broader “what to expect” guidance, this payment security best practices guide also helps connect rules, standards, and real-world protections.

One key gotcha: security doesn’t always look like “more steps.” Sometimes it looks like fewer prompts because systems trust a device or payment context more.

So, it’s normal if you sometimes see extra authentication and other times you do not. It depends on risk and the card brand rules.

Here’s a good rule of thumb:

If something looks off, your bank or card network may pause the payment. That pause protects both sides.

When you understand the payment phases, security makes more sense too. Authorization checks risk right away. Then encryption, authentication, and fraud tools protect the path while funds settle.

At this point, you can see how the system balances speed and safety. Now let’s land the big takeaway.

Your Payment’s Journey, in Plain Language

Your question was simple: how does a payment move from your account to a seller? The answer comes in four steady phases: authorization, clearing, settlement, and payout.

Cards often feel instant at approval, but settlement can take days. ACH can take longer, but it may cost less. Wallets speed up checkout and may route through different underlying rails.

Finally, 2026 is pushing more payments toward real-time settlement. FedNow and RTP are expanding, so more businesses can receive cash faster.

If you ever wonder why a payment is delayed, it usually comes down to clearing and settlement timing. If you want true instant payments, check whether your bank supports real-time rails.

- Why does my payment show “pending”? Often it’s authorized, but settlement hasn’t finished.

- Can payments be instant in the U.S.? Yes, when real-time rails are used and both sides support them.

- Will security slow me down? Sometimes it adds steps, but better authentication can also reduce friction.

Next time you buy coffee, your money will still follow the relay race. But now you’ll know the runners and why the baton reaches the seller when it does.